Quick Answer: How Much Cyber Insurance Do I Need?

The need scales with your business

1/16/20262 min read

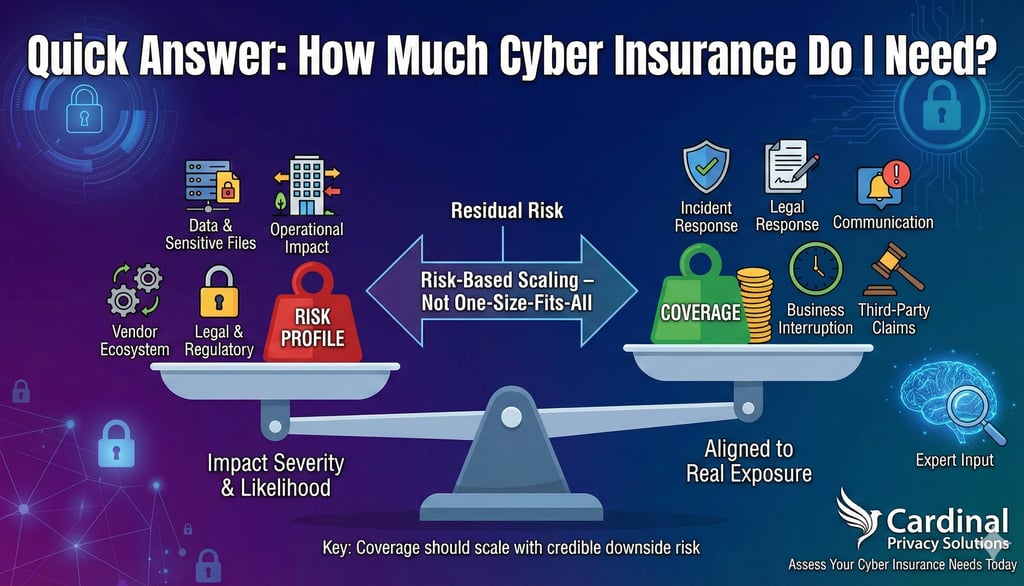

There is no universal answer to how much cyber insurance an organization “needs.” The appropriate amount of coverage depends on your specific risk profile, not on generic benchmarks or what peers claim to carry. Cyber insurance should be scaled based on the realistic likelihood and potential impact of cyber incidents affecting your organization, not treated as a one-size-fits-all purchase.

At a high level, cyber insurance is designed to transfer residual risk—the risk that remains after reasonable security, privacy, and governance controls are in place. Determining how much coverage is appropriate requires understanding both what could go wrong and how bad it would be if it did.

Start With Risk-Based Scaling

A risk-based approach focuses on two core questions:

Impact severity: If a cyber incident occurred, what would the operational, legal, regulatory, and reputational consequences look like?

Likelihood: Given your data types, systems, vendors, and threat landscape, how probable is a meaningful incident?

Organizations that process sensitive personal data, rely heavily on digital operations, or have complex vendor ecosystems generally face higher potential impact. Conversely, organizations with limited data exposure and strong internal controls may justify lower limits. The key is that coverage should scale in proportion to credible downside risk, not aspirational worst-case scenarios.

Align Coverage to Real Exposure

Cyber insurance policies vary widely. Coverage limits should be aligned to realistic costs such as:

Incident response and forensic investigations

Legal and regulatory response obligations

Notification and communication requirements

Business interruption and recovery

Third-party claims arising from data exposure

Over-insuring can be as inefficient as under-insuring. Excess coverage that does not map to plausible loss scenarios adds cost without materially improving resilience.

Why Expert Input Matters

Assessing impact and likelihood is not purely an IT exercise. It requires a multidisciplinary understanding of privacy obligations, regulatory exposure, vendor risk, and operational dependencies. This is where an experienced fractional privacy officer adds material value.

A fractional privacy officer can objectively evaluate:

The sensitivity and regulatory profile of your data

How privacy and security controls reduce or fail to reduce exposure

Where insurers’ assumptions may diverge from operational reality

Whether proposed coverage aligns with actual risk drivers

Their role is not to sell insurance, but to ensure insurance decisions are grounded in defensible risk analysis rather than guesswork or fear-based purchasing.

The Bottom Line

You need enough cyber insurance to cover the realistic impact of incidents your organization could plausibly experience—no more and no less. The most effective way to arrive at that number is through a risk-based assessment informed by privacy, security, and governance expertise. When coverage decisions are guided by structured risk analysis and expert judgment, cyber insurance becomes a strategic risk-transfer tool rather than an expensive uncertainty hedge.

Reach out today for Cardinal Privacy Solutions to assess your cyber insurance needs.

Contact

Reach out for tailored privacy and security guidance

peter@cardinalprivacy.com

© 2025. All rights reserved.

Website Privacy Notice: This website is operated only on a business-to-business basis and is out of scope for California Privacy Regulations due to the size and nature of the operator.